Buyer

Navigating the world of home financing can be a complex task, especially when it comes to understanding the various types of mortgages available. At The Keystone Team, we believe that a well-informed buyer is an empowered one. In this comprehensive guide, we'll break down the different types of mortgages, helping you choose the right one for your unique needs.

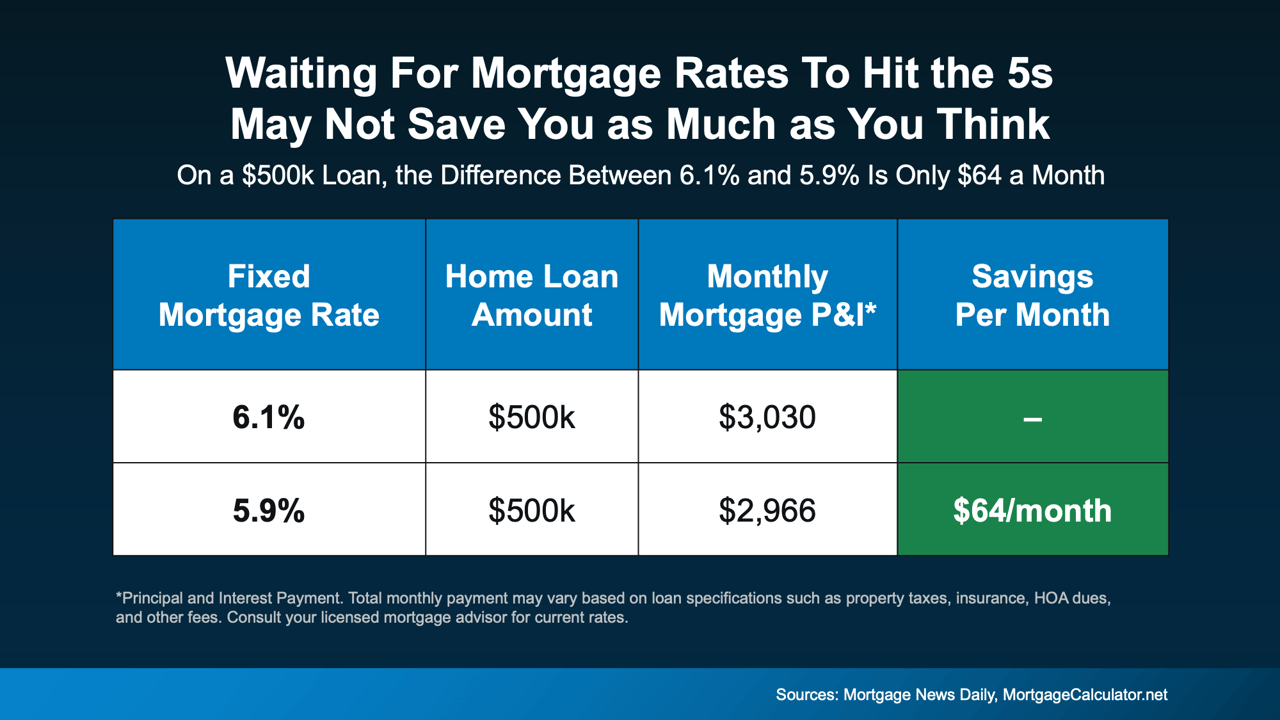

Fixed-rate mortgages are the most common type of home loan. As the name suggests, the interest rate on a fixed-rate mortgage remains constant throughout the loan term. This means your monthly payment stays the same, which makes budgeting easier.

With an adjustable-rate mortgage, the interest rate can change over time, typically after an initial fixed period. This means your monthly payments could increase or decrease. ARMs can be beneficial if you plan to sell or refinance your home before the rate changes.

Insured by the Federal Housing Administration, FHA loans are designed for low-to-moderate-income borrowers. They require lower minimum down payments and credit scores than many conventional loans.

If you're a veteran, active-duty service member, or eligible spouse, you might qualify for a VA loan. Guaranteed by the Department of Veterans Affairs, these loans often come with favorable terms, such as no down payment or mortgage insurance requirement.

USDA loans are backed by the United States Department of Agriculture and are designed to help rural and suburban homebuyers. These loans often require no down payment and offer below-market interest rates.

Jumbo loans are used to finance luxury properties and homes in highly competitive local real estate markets. They exceed the conforming loan limits set by the Federal Housing Finance Agency, meaning they can't be guaranteed or insured by the federal government.

With an interest-only mortgage, you only pay the interest on the loan for a specific period. After that, you'll start paying both interest and principal. These loans can be useful if you expect your income to increase in the future.

Balloon mortgages require you to make regular payments for a certain period and then pay off the remaining balance in one large (or "balloon") payment. While this can lower your monthly payments, it's crucial to ensure you can afford the balloon payment when it's due.

Choosing the right mortgage is a crucial step in your home buying journey. At The Keystone Team, we're here to guide you through this process, providing expert advice tailored to your unique needs. With our comprehensive support, we'll help you secure the best mortgage, making your dream of homeownership a reality.

Stay up to date on the latest real estate trends.

Real Estate

Real Estate

Real Estate

Real Estate

Real Estate

Real Estate

Real Estate

Real Estate

Real Estate